The Ministry of Finance has issued Federal Decree-Law No. 18, are you ready to face the changes in the UAE VAT? BMS Auditing helps you to face all VAT Challenges!

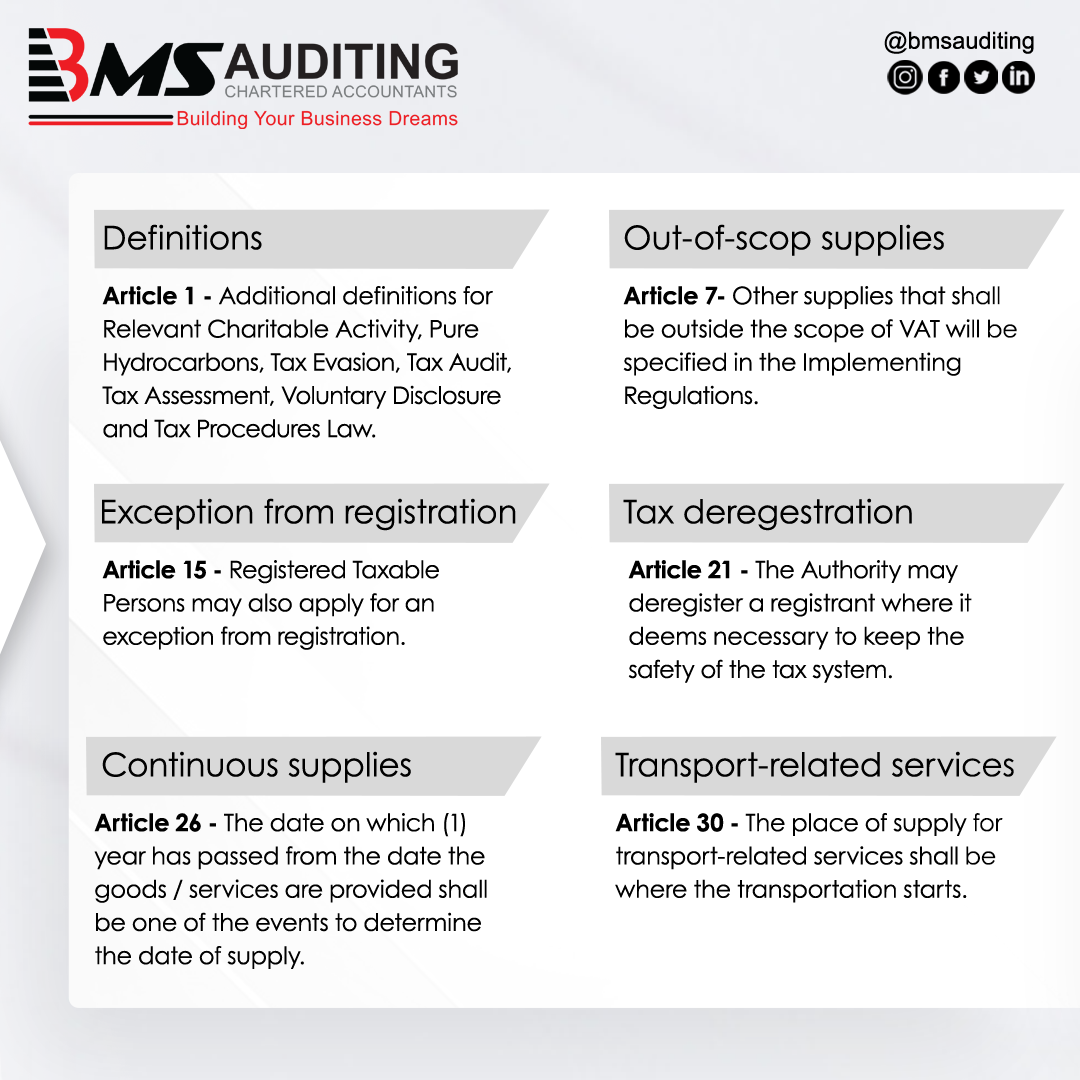

The Ministry of Finance has issued Federal Decree-Law No. 18 of 2022 amending various sections of Federal Decree-Law No. 8 of 2017 on VAT (the Amendment Law). Effective from January 2023, registered taxable persons would be allowed to apply for an exception from VAT registration, provided all their products are Zero-rated.

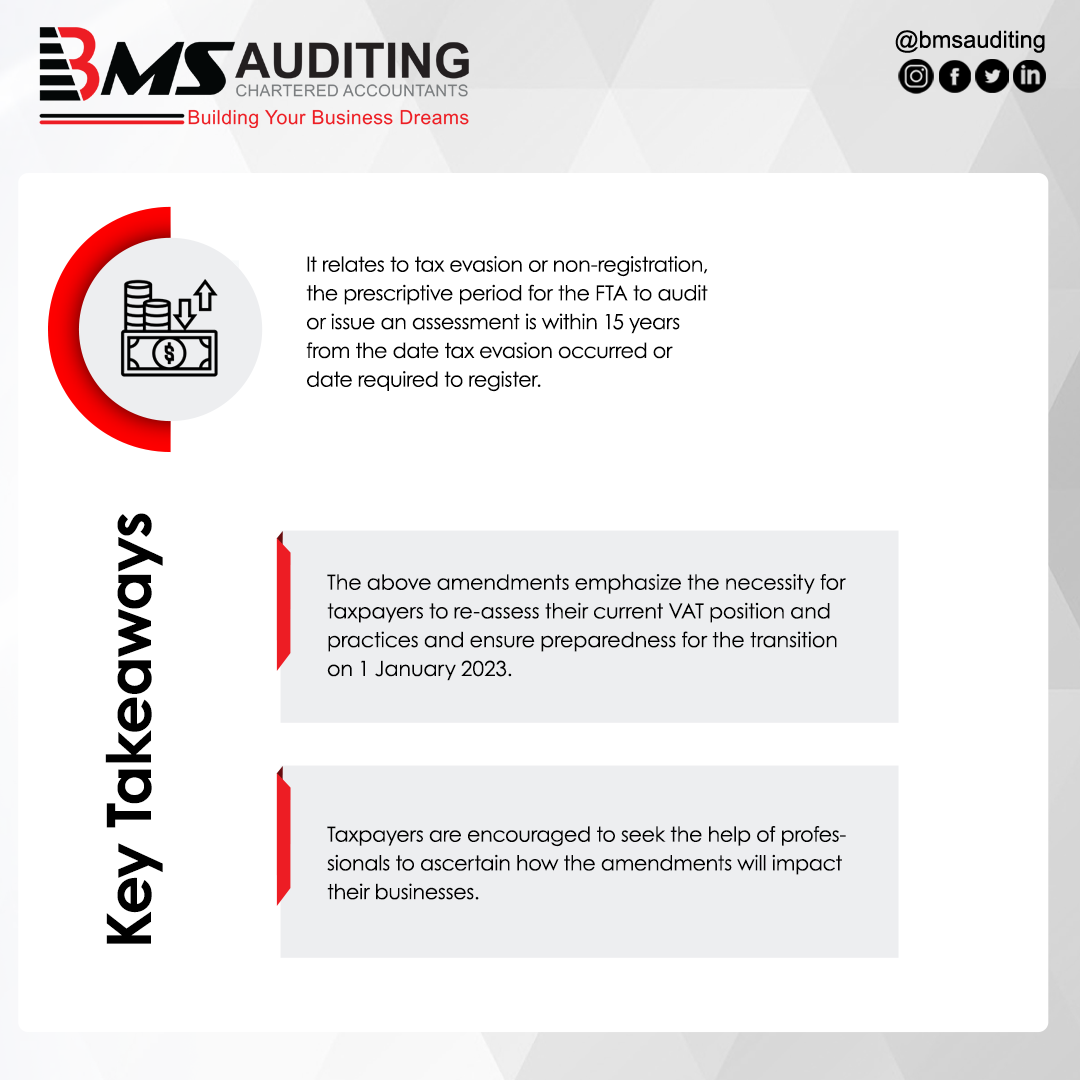

New Changes in VAT

The Amendment Law modifies some provisions of Federal Decree-Law No. 8 of 2017 on VAT, which takes effect on January 1, 2023. There are also changes in certain features to clarify and state the prospective meaning of the content; revise or refine the legislative series of legal conditions. There were no significant changes brought in the VAT rate, which means it remains constant at 5%.

The following are some of the key changes:

Tax exemption for zero-rated goods

One of the changes made to the Federal Decree-Law No. 8 of 2017 on VAT, is the term that the registered persons would be allowed to request an exception from registering for VAT if all their products are zero-rated or they are not producing any items other than the zero-rated products. If a registered person makes zero-rated goods and does not make (or no longer makes) standard-rated supplies, they may seek a VAT registration exemption.

The Zero-rated products come under the category of taxable property and services at 0%, for instance, foods and beverages, exported goods, donated goods from charity shops, equipment for the disabled, and prescribed medications, and evaluated by the taxing authority.

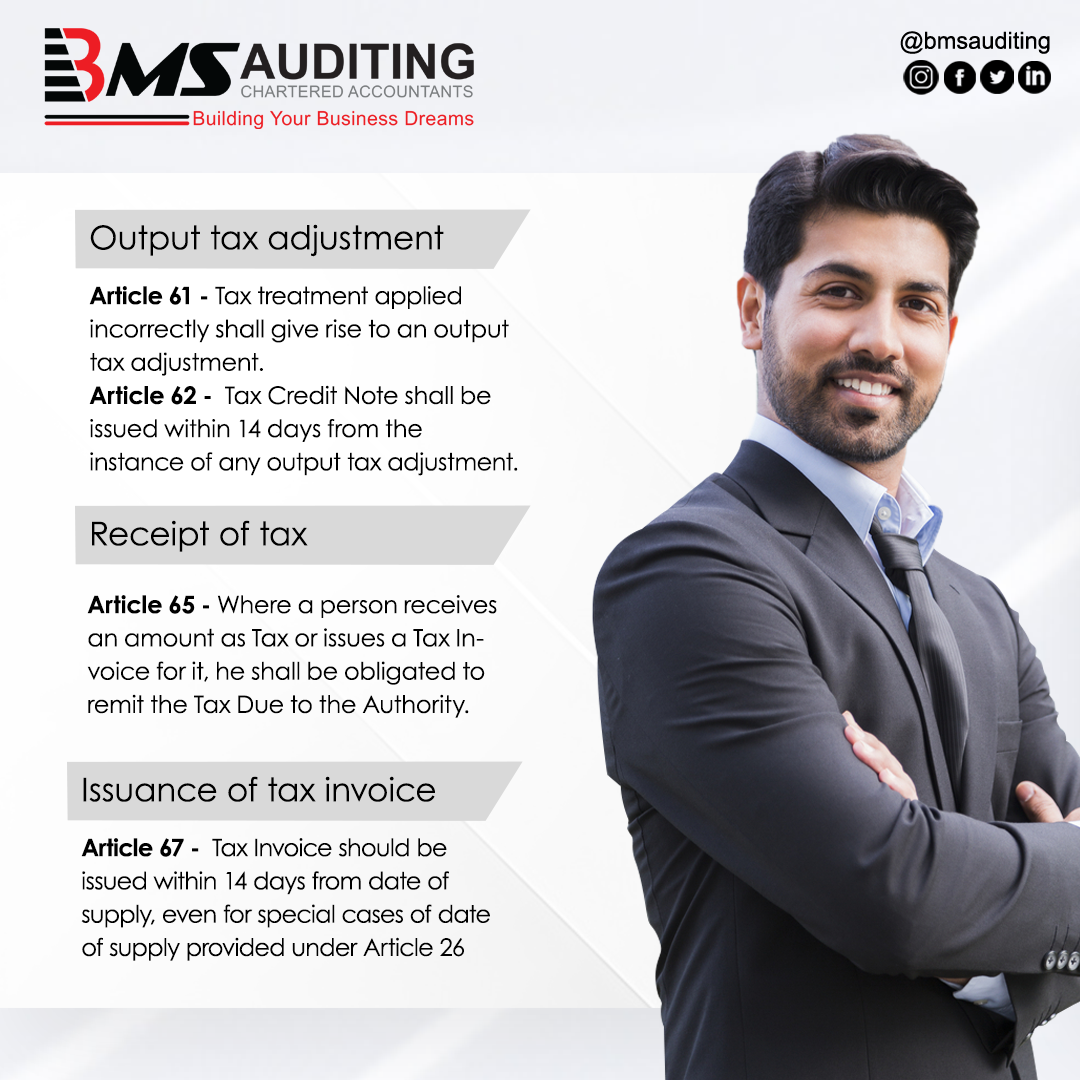

14-day time limit for Tax Credit Notes.

Besides these major amendments, there are changes such as setting a 14-day period for issuing a credit note. Setting a 14-day time frame for issuing a Tax Credit Note to settle output tax, which corresponds to the same time frame for issuing Tax Invoices. The ministry stated that the Federal Tax Authority (FTA) might compulsorily deregister the persons in critical cases if necessary.

FTA may deregister VAT if needed

The Federal Tax Authority (FTA) may forcefully deregister registered people if considered necessary. Furthermore, the Decree-Law contains revisions to specific parts in order to clarify and confirm the intended meaning of the text; to rewrite the language, or to better the legislative sequence of legal laws.

Complete Updated Federal Decree Law

BMS Auditing compiled all the Federal Decree Law released by the Ministry of Finance and listed the changes in detail below.

The statement added that the changes were made corresponding to the international best practice, after the GCC Unified VAT Agreement. These changes were based on the experiences, challenges faced by business sectors, and suggestions received from relevant people.

BMS Auditing UAE has reliable VAT consultants in Dubai whom you could always look up to when you have queries. Our consulting team assists with regular updates on VAT and VAT Rates from the FTA.

Need more help? Have queries? Call BMS.