What is VAT Reverse Charge Mechanism (RCM)?

Reverse Charge Mechanism (RCM) under VAT eliminates the responsibility for the businesses outside the UAE to register for VAT in UAE. The reverse charge mechanism under VAT is mainly used for transactions from cross the border.

In a typical business, the supplier supplies goods to the customers and collect VAT from the customers, which is later paid to the Federal Tax Authority (FTA). Under reverse charge mechanism (RCM), the supplier does not charge VAT to the customer, the buyer or end customer pays the tax directly to the government authority.

The supplier does not have to pay VAT on import items, so the obligation of reporting a VAT transaction is shifted from the seller to the recipient. The recipient will have to record the VAT on purchases (input VAT) and the VAT on sales (output VAT) in their VAT return each quarter.

If the supplier is from outside the country and does not have a business in the UAE, the VAT does not implement on the businesses who are not in UAE. Hence, recipients who are residents of the UAE and receiving goods from the supplier who is not in UAE are made to pay VAT on reverse charge basis.

Applicability of Reverse Charge Mechanism Under UAE VAT Law

Reverse charge is applicable in the following cases:

- Import of goods/services from other GCC and non-GCC countries. The supplier of these goods/services must be located in another country and they may or may not have a business in the UAE.

- Purchase of goods from a designated zone

- Supply of gold and diamonds

- Purchase of gold and diamonds for resale or further production/manufacture

- Supply of hydrocarbons for resale by a registered supplier to a registered recipient in the UAE

- Supply of crude/refined oil by a registered supplier to a registered recipient in the UAE

- Supply of processed/unprocessed natural gas by a registered supplier to a registered recipient in the UAE

- Production and distribution of any form of energy supplied by a registered supplier to a registered recipient in the UAE

How does reverse charge mechanism on services work?

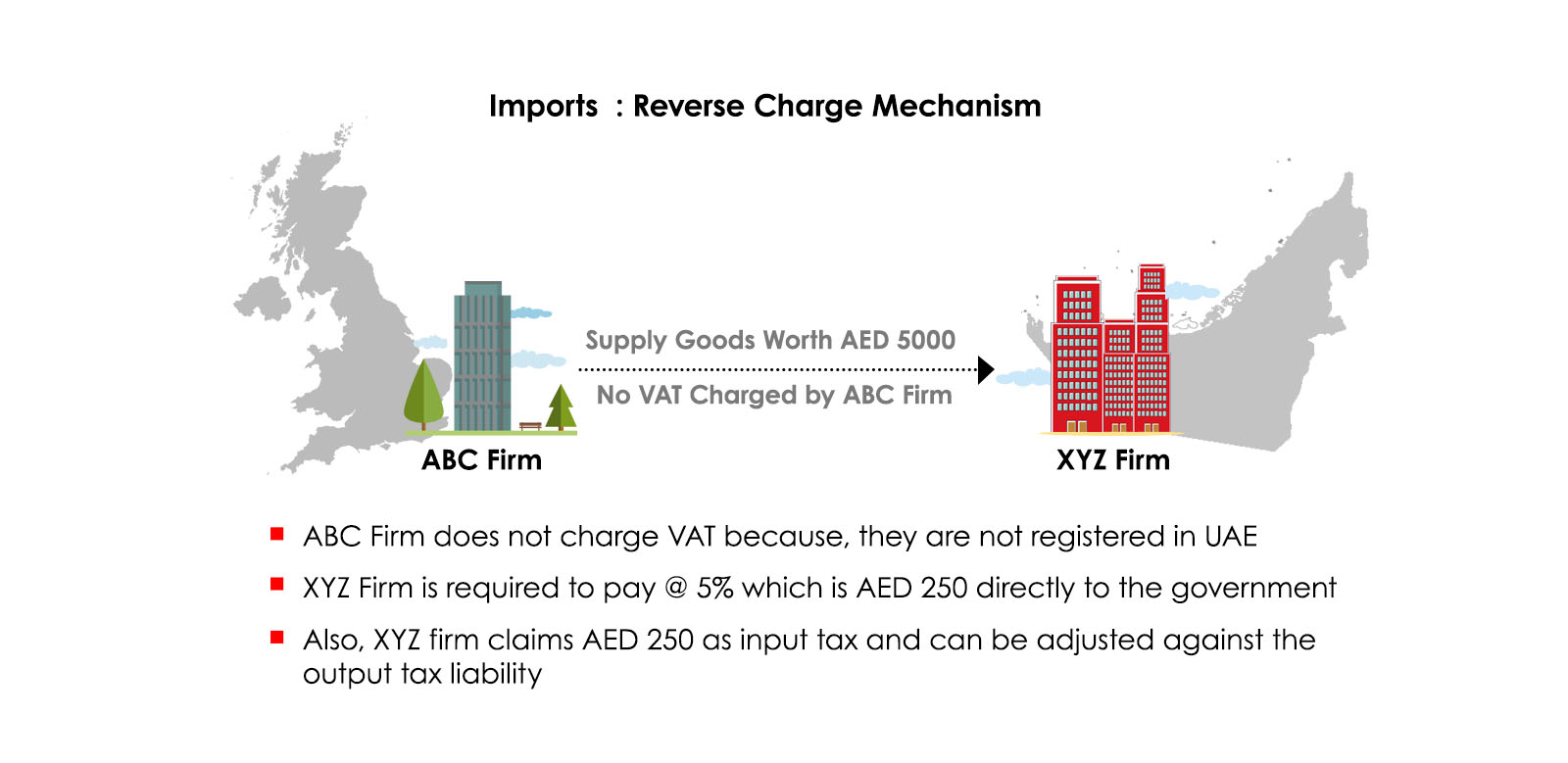

To understand the concept of reverse charge mechanism under VAT in UAE, let’s look at an example using an imported products:

XYZ is a VAT-registered firm in UAE, they are importing goods from an ABC firm which is in UK. As ABC firm is not registered in the UAE, they do not have to file any UAE returns or pay UAE tax. Because ABC firm in UAE has acquired products from a non-UAE-based supplier, they will have to record the reverse charge on their relevant VAT return. In this example, because the recipient accounts for the VAT under the reverse charge mechanism, the place of supply for VAT purposes is the UAE.

The conclusion of the above mentioned example is that the net result of reverse charge mechanism is same as that of forward charge basis.

The only difference in reverse charge VAT is the shift in the responsibility of paying VAT which is moved from supplier to the recipient.

In the above illustration, it is moved from ABC Firm to XYZ firm. In a way, the concept of reverse charge mechanism helps to alleviate the difference between local and international suppliers and puts both into the same position.

How would recipients deal with the reverse charge transaction?

Businesses should calculate the amount of tax to be paid to the Federal Tax Authority (FTA), self-account the VAT amount as output tax during the purchase and then declare it in their VAT return. Businesses may claim input credit if possible. Make sure you maintain the necessary documents like invoices for future reference.

What are the requirements for the reverse charge mechanism?

- The receiver of the goods or services must be registered for VAT.

- Every registered business owner must keep proper records of their supplies that incur reverse charge.

- Invoices, receipt vouchers, and refund vouchers should all specify whether the tax payable for that particular transaction is through reverse charge.

How and when to use the concept of Reverse Charge Mechanism (RCM) is a complex question and it needs professional and experienced opinion to define the mechanism as per the VAT law in UAE. BMS Auditing is authorized Tax Agent by Federal Tax Authority (FTA) who can help you in understanding the concept of Reverse Charge Mechanism under VAT.

If you are looking for any clarification in terms of RCM VAT in UAE, Contact BMS Auditing Dubai. We are covering all the elements of VAT such as VAT registration, VAT return filing, VAT audit, VAT refund, VAT accounting and VAT deregistration.

FAQs

1. Are the suppliers from the free trade zone treated as foreign suppliers in reverse charge mechanism (RCM) transactions?

Yes, companies from the free trade zone supplying goods and services to anyone in mainland UAE are treated as foreign suppliers.

2. If I imported items from a foreign country in one taxable period, but I resold them in another taxable period when do I have to pay VAT through RCM?

You must pay VAT through RCM at the time of importing goods from a foreign country to the UAE.